|

10 Steps to Become a Millionaire

Originally Published in Fulton Living Magazine

Americans can become millionaires in many ways – including real estate, business, inheritance, etc. However, I believe the surest path for most Americans is simply by saving and investing, and effectively using your company’s 401k plan. So here is a clear 10-step path to joining the ranks of America’s 401(k) millionaires:

Sign up for your 401k and do it TODAY.

If your company offers a match, ALWAYS contribute at least the full match, because it is an instant 100% rate of return. For example, to get a 3% match from the company, you need to contribute 3%, which is a 100% rate of return. Irrespective of market performance, the company is putting in for you the same amount that you are. ALWAYS CONTRIBUTE AT LEAST UP TO THE MATCH, it’s hard to beat from a rate of return perspective.

After you are putting in the minimum to capture the maximum match, save as much as you can. The only caveat here, is if you have other more important short-term priorities or financial obligations. For example, if you need to put extra money towards buying a new home, or medical expenses those may take priority. Or if you have high interest debt, like credit card debt at 15%, it may make more sense to pay that off before putting extra money into the 401k. Once those are paid off, redirect what you were paying towards those expenses or higher interest debt into the 401k!

Take 20 minutes to see if a Financial Planner or CPA can help determine if you are better off using a Roth 401k or a Traditional 401k – the difference in taxes between now and later can really make a difference.

Focus on your asset allocation and investment mix and start with a bias towards growth and stock allocation. Too many 401k investors hold far too much of their account in bonds, which should be kept to a minimum for those trying to accumulate long-term wealth. To get to millionaire status, you will need to be more of a stock owner, not a bond lender.

Don’t market time! Every time you get paid, invest each pay period, no matter what is happening in the markets! IGNORE THE NOISE! Don’t pay attention to the up and down movement of your account. Make automatic contributions each pay regardless of how the market is doing right now.

If you have the cash flow to do so, accelerate your contributions as early in the year as possible. For example, if your plan is to max out your 401k for the year, and you can do it in 6 months instead of 12 months, this gives your money more time to grow. However, before doing this, check with your HR representative to ensure that you won’t lose any of your company match by doing this.

Pay attention to costs of the funds and get familiar with the costs of each funds and have a bias towards lower cost funds.

Utilize funds that represent indexes. For example, you could incorporate funds that represent the S&P 500 index or International Indexes. Make sure you have diversification across the main asset classes – Large Cap, Mid Cap, Small Cap, International Developed Markets, International Emerging Markets, Real Estate, Commodities.

Wait until you reach full retirement age (at least 59.5 years old) to withdraw your funds, so you won’t pay a penalty for an early withdrawal. Let tax-deferred compounding work for you as long as possible!

If you follow these tips, for a few decades, it is almost certain you will become a millionaire!

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra IS or Kestra AS. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by Kestra IS or Kestra AS for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security.

On It with Offit - August 2022

|

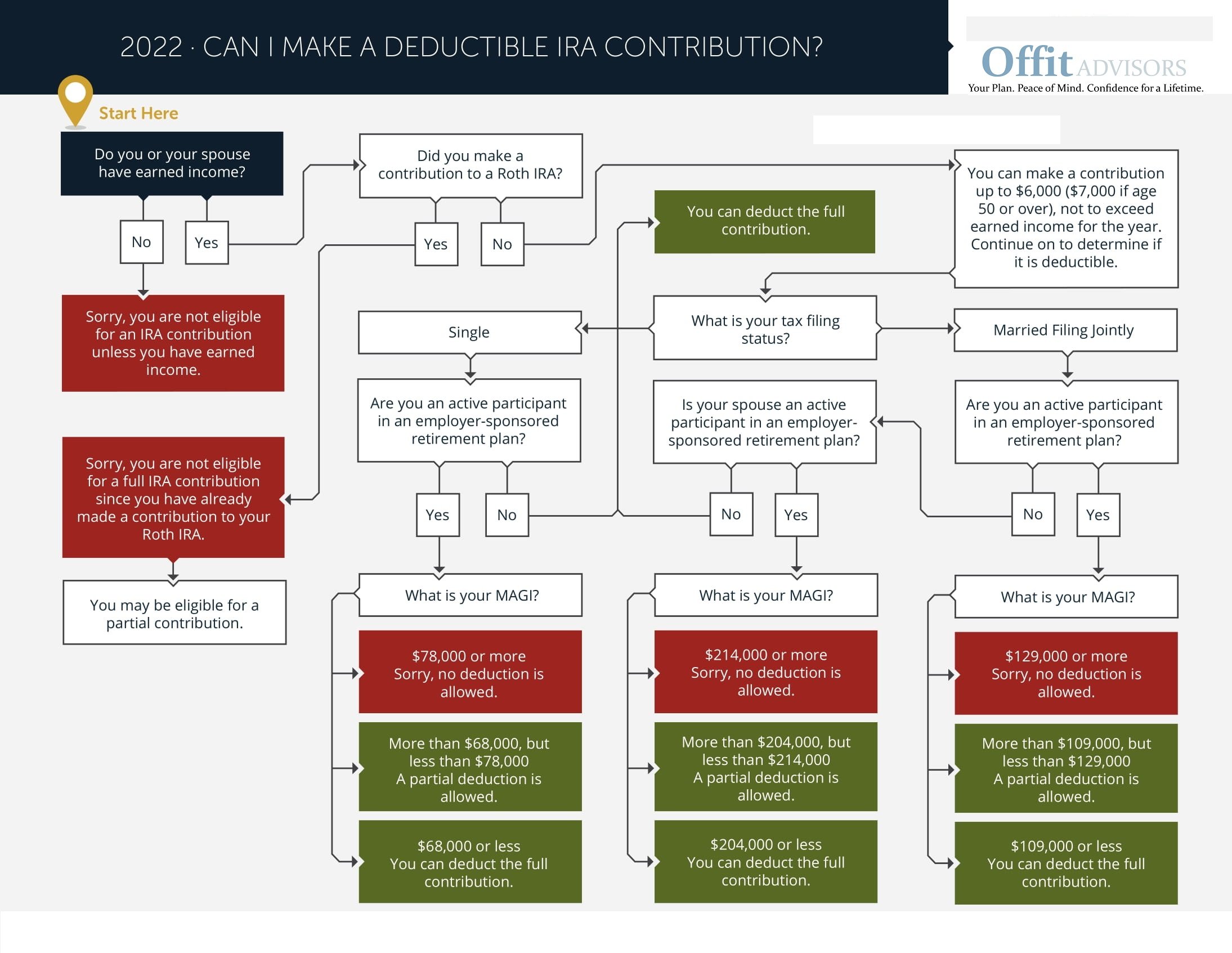

Can I Make a Deductible IRA Contribution?

As financial advisors, we sometimes see mistakes in contributions to IRAs and Roth IRAs. While saving for your retirement is a good thing, you want to be mindful of the rules and doing it correctly.

An unfortunate mistake we see sometimes is people contributing towards IRAs and being fully aware that their deduction may not be eligible based on various reasons. Typically if one has a retirement plan at their job, that is the best place to get a tax-deduction because it is not contingent upon other factors like an IRA can be.

This chart can help explain the various paths to determine if your contribution is actually eligible for a deduction.

Money and Your Financial Purpose

I have often seen some of the best financial planning clients – the ones who save and invest regularly, protect their assets, care about their futures and families, and are meticulous about being on track with their finances, and struggle to transition into retirement.

They have done a tremendous job and deserve credit for putting themselves in the fortunate financial position they are in. They have saved and lived within their means for so long, so starting to spend and use their money that they have accumulated feels so foreign to them. They aren’t necessarily depriving themselves, but they aren’t necessarily enjoying their position to the fullest either.

But the reality is that none of us will live forever, and everyone’s day will eventually come, and no one gets a reward for being the richest person in the graveyard. There are also many people who may have an underlying feeling or inkling as to what their purpose in life is or how they may want to use their money, but they don’t fully pursue it. I feel there are many people who are fortunately successful with their money, but they also need to be more successful in not missing their opportunity to live their lives and enjoy a life of significance, right now!

I believe part of my role as a Financial Planner and Advisor for clients is to help them utilize their money as a tool to help them enjoy life and realize their life’s purpose.

It’s their money, they have busted their butt to earn, save, and grow it, and as long as they are not jeopardizing their own financial security, they deserve to enjoy their money and utilize it towards fulfilling their life’s purpose today.

If one reaches the point of financial security and can afford to utilize their money, while not disrupting their financial independence, they should strive to take advantage of their position and look for daily opportunities to enjoy life, pursue their dreams, and live their purpose. For example:

If you want that extra tall coffee at Starbucks, go get it!

If you have always dreamed of going to Fiji, go now!

If you have always wanted to help your Son or Daughter launch a business idea that they have had but couldn’t afford to pursue it, help them now!

If you have always wanted to help end poverty or end cancer, do something about it today!

If you or someone you know may fit this description, please share that you have worked hard to climb up to the mountain top, and hopefully you have had a great guide or Advisor along the way to help you reach the Summit. Enjoy your journey along the way to the top, but also don’t forget to enjoy the view once you get there.

A Simple Truth; Stay Invested.

Hello Loyal Readership!,

Today I want to discuss some cliché but truthful facts about the market and keep it simple.

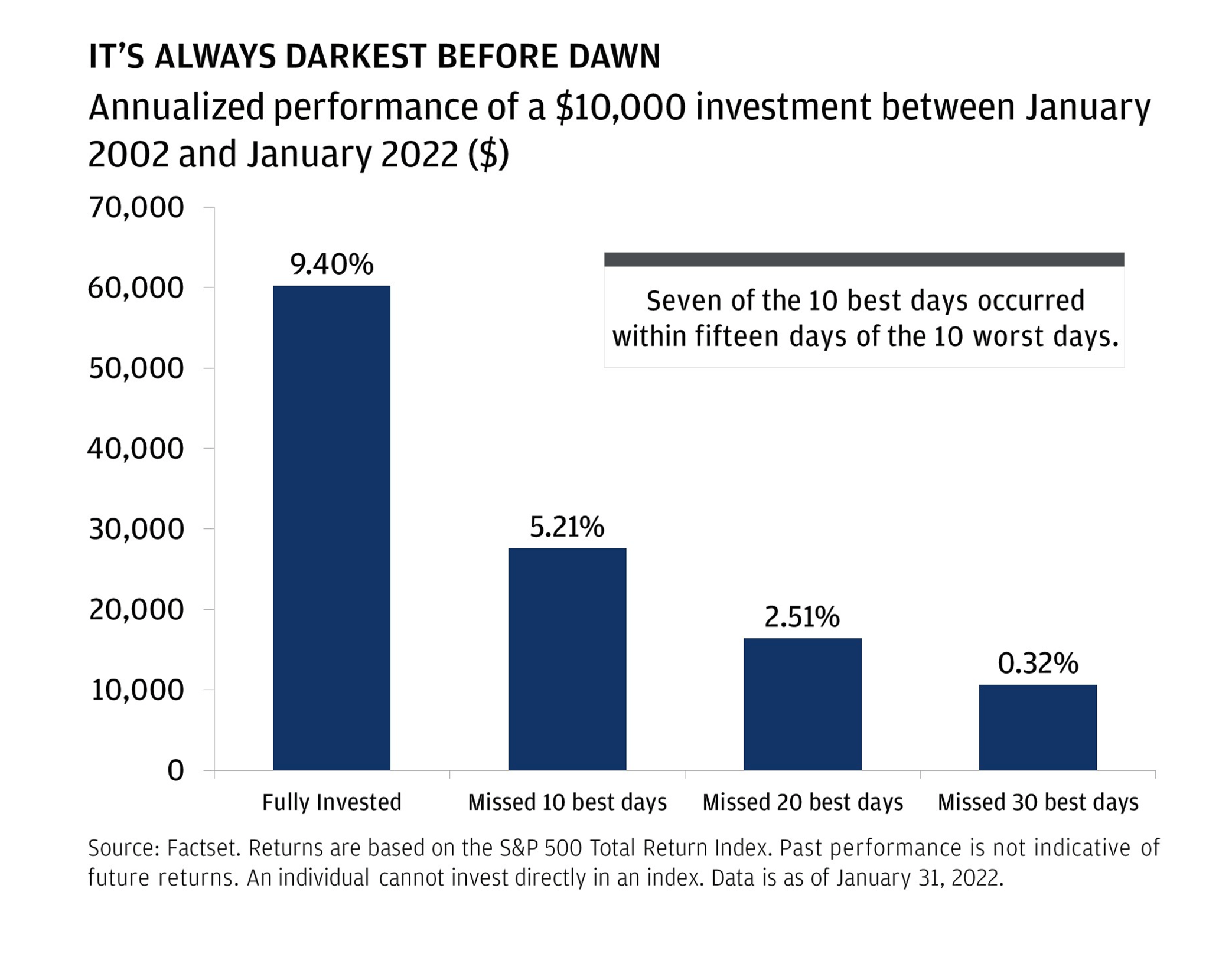

If we look back and we look forward, history has shown us that market continues to rise over time, but it is not a straight line, it is a wavy line. I fully expect this trend to continue in the future. Take a look at the graphic below illustrating various domestic, global, and economic events we have been through, but despite all of these unnerving moments the market continues to rise over time and someone who had invested $1 in the S&P 500 in 1970 would have $80 in 2021 just by staying invested.

A disciplined investor looks beyond the concerns of today to the long-term growth potential of markets.

The problem is most investors get in their own way. They see the current investment “apocalypse du jour” and react. This is not to not be sensitive to whatever the event that is going on – these are real events affecting people’s lives, but just not their long-term portfolio. For example, when oil prices quadrupled in the mid-70’s many investors were tempted to exit the market and “cut their losses”. But those that don’t get in their own way experience the gains that the market features by just saddling in and riding for the long term. As you can see in the graphic below, over the last 20 years, the “average investor” only received a 2.9% rate of return while the S%P 500 did 7.5%.

The final piece I want to share as to why you need to stay invested is because the best days occur without warning, often near the worst days. So if you ride out the worst days, you will subsequently closely capture the best days. But if you miss the best days, that has a lasting impact on your growth.

Stay invested. It’s a simple truth.

Taking Advantage of Market Volatility

Hello Loyal Readership!

I hope this message finds you well today. I know that no one enjoys the volatile periods of market, but if looked at through a different perspective, once can actually use this to your possible positive financial planning advantage!

Here are some of the top to tips to consider in a down financial market, AKA – right now!

1. Roth IRA conversion – if you have the opportunity to convert some of your pre-tax accounts into post-tax accounts and pay the tax now, but never pay the tax again, this could be an opportune time to do it. If you do it today, and convert now with lower values in your portfolio, you would pay tax on a lesser dollar amount today in exchange for a future earnings on your portfolio to never be taxed again.

2. Tax loss harvesting – if you have a non-qualified (non-retirement account) you can sell out some of your holdings that may have taxable losses and buy something similar but not the same and put a loss on your tax return. This can help you offset any positive gains in your portfolio that you would otherwise have to pay tax on.

3. Rebalance your portfolio – sell what may be high in your portfolio and buy back into what is low ie. If the designed allocation on your portfolio featured 80% stocks and now stocks represent only 62% of your portfolio, you can rebalance now instead of waiting

4. Contribute and invest more now! – with market values being lower today than they were just weeks ago, this is a buying opportunity to buy securities at a discount and “on sale”. Who doesn’t like to buy things on sale?

5. Appreciate the value of being diversified – over recent years with the S&P 500 and tech stocks being the top performing asset classes, people would say there are no need to own other asset classes. The value of having a broadly diversified portfolio with other aspects to diversification is being demonstrated now. For example, energy was one of the worst performing asset classes of the last decade, but this year it is the biggest winner. If you have a diversified portfolio there can be segments that do better than others in different market cycles.

7. Non-market correlated assets – there is value to having some parts of your overall wealth strategy in buckets that are non- market correlated – meaning that they don’t go down when the market goes down. This is especially true of those who are very near to approaching retirement.

7. Front- load, if you can – if you have the opportunity to put more into your 401k at your job or your IRAs or Roth IRAs, now is a great time do it. Why not put more in now when share prices are more on sale!

8. Speculative investment fads are showing they were just fads! – Crypto, NFTs, SPACs – we have said it here and will say it again most of these will go to zero. If you got caught up in the hype over the past couple of years, now may be a time to re-think and re-position your strategy now and moving forward.

If you found any of this helpful, or have questions about any of the above strategies, please let us know and we will be glad to help you.